This blog summarizes some original research done in the 1990s that is probably still relevant to federal cost accounting use today. It was published as "Motivating Contingencies at Early Adopters of Federal Cost Management Accounting Systems," The Government Accountants Journal, Spring 1995, Volume XLIV, No. 1.

The research was part of my doctoral thesis and started with the generous sharing of data by the General Accounting Office (now Government Accountability Office). They had surveyed federal agencies on the existence and use of cost accounting. Fifty nine agencies responded to the survey.

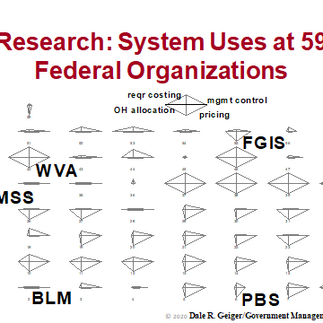

Statistical analysis of system use general the chart shown in the illustration. The diamonds represent the degree of use along four axes. Starting at the top and going clockwise these are required costing, management control, pricing, and overhead allocation.

I then conducted field research at five of the organizations to better understand the statistical results.

Bureau of Land Management (BLM)

I looked at the Fire Management Services: an organization that provides fire prevention and suppression for ten western states and Alaska. They had no requirement for costing or pricing as they were an appropriated organization. Their cost accounting was, however, needed for reimbursement purposes.

A fast response is critical when a fire starts and there is not time to seek budgetary funding. When a major fire breaks out BLM has the authority to use cash from available accounts. Cost tracking is then used to justify supplemental funding replacement after the fire.

Fire operations also used costing to charge operations for equipment maintenance and replacement. The funds for replacement of fire engines, for example, were then available when needed. Centralizing the charge for maintenance also motivated operations to have the maintenance done rather than postponed by the need for competing budget uses.

Veterinary Medical Services (VMSS)

Veterinary Medical Services was part of the National Institutes of Health. It, and the following four organizations was revolving funded. This means they received no appropriated funding and operated like businesses. They received revenue from products and services and had a profit goal. The major difference from a business was that their profit goal was zero.

Medical Services charged other departments at the Institute for providing any of thousands of research supplies. These included, for example, many, many difference types of specially bred mice with genes that made them good test subjects for specific research protocols.

This service facilitated the Institutes’ research by providing high quality materials at competitive prices since researchers were not obligated to use the VMSS. Medical Services tracked costs and used them to adjust their published prices as needed.

Federal Grain Inspection (FGIS)

The Federal Grain Inspection Service was part of the Department of Agriculture. It charged fees to shippers for inspecting grain shipments and assuring that grain met federal standards.

Fee revenues were tracked against cost. If the balance in the residual account fell too low the fee was raised. Reaching the upper limit similarly triggered a fee reduction.

Watervliet Arsenal (WVA)

The Arsenal was a government owned, government operated manufacturing facility of the United States Army that made cannons. It also was a revolving funded organization dependent on cash inflow from other military unit’s purchases and from foreign military sales. Their requirement was for revenue from sales to cover manufacturing costs plus or minus 1.5%

With complex machining and heat treating processes and costly assets the Arsenal needed an equally complex dual standard cost system. They needed to track and allocate costs to products in order to avoid under or over pricing sales.

Public Building Service (PBS)

Building Services owned and managed over 5000 federal buildings as part of the General Services Administration. They also received no appropriations and charged federal tenant organizations a market based rent.

The “rents” charges also included the costs for a “standard level” of services such as security or reception. Costs for tenants who needed extra services were tracked on a project basis. PBS’s cost accounting system tracked all costs by building and provided monthly profit and loss statements.

Takeaways

The five cases studies indicated great diversity in approaches to cost accounting as dictated by the operational requirements of the organization. However, all had one compelling reasons to track cost: their cash inflow depended on it.

Commenti