Level of effort analysis is one method to determine a driver for the basis of allocation. The basis of allocation is used to establish a rate or proportion that distributes cost to the organizations, operations, or outputs of an organization.

Allocating Quality Control at the IRS

One of my research projects was conducting an experiment at the Boston District of the Internal Revenue Service. The experiment involved building an activity based costing model that would determine the costs of the various audit programs at the IRS.

One of the overhead or support organizations at the District Headquarters was Quality Control. Their job was to sample and review audit work to ensure it met standards for high quality.

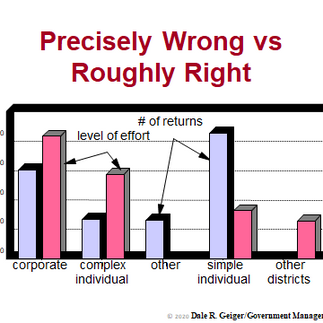

The cost objects were five major categories of audit programs. One program handled all corporate tax returns. Another looked at complex individual returns that typically included partnerships or sole proprietorships. The greatest volume of returns consisted in the category of simple individual returns. “Other” included miscellaneous return, payroll tax issues, inheritance, etc. The last category of interest was work done for other districts.

The question was how the cost of the Quality Department should be allocated or distributed to these five programs. The initial recommendation of management was to use the number of returns in each category. That was a distribution that was known with great accuracy and great precision was perceived as highly desirable.

However, the goal of the project was to evaluate the cost of the various audit programs and that goal implied that there needed to be a cause and effect relationship built into the driver selection. Using number of returns as the driver suggests that more returns causes more quality control. Another way to state this assumption would be that all audits took the same amount of Quality Control cost regardless of type of audit. These assumptions did not seem to be reasonable as many returns were “simple” and therefore not require much audit effort.

This is a common problem in driver selection when considering use a “number of” metric. The metric will not capture an underlying cause and effect relationship unless the “number of” are very similar in complexity. If there is any systematic complexity difference the choice of a “number of” driver will distort the resulting cost distribution.

Level of Effort Analysis

We decided to conduct a level of effort analysis to build a driver basis of allocation customized to the Quality Control Department. Level of effort (LOE) required interviewing the Quality Control manager to determine where her people’s efforts (ie. costs) were being spent.

This interview was the first time the question had ever been asked and she was initially hesitant and stated that there was no accurate time keeping system to inform her. So we went through her staff of ten or twelve and talked about each’s job responsibility. It quickly became clear that most people specialized in one or two of the audit programs’ audits and she was comfortable estimating how each person’s time was spent.

Once we had the matrix of effort by person we made the assumption that salaries were roughly equivalent. Summing the matrix gave us a reasonable reflection of where the department’s efforts and therefore costs should be allocated.

The illustration shows the comparison between two drivers. One is the “number of returns” driver and the other is LOE. The comparison showed a dramatic difference that made sense to the District’s senior management team. It was clear that the complex individual and corporate returns absorbed the bulk of the Quality Department’s time. They simply required a lot more time per audit.

The other “surprise” to the team was that “other” districts were consuming a fair amount of resources. Since these returns were not counted in the Boston District the “number of returns” driver completely misplaced this cost. The LOE analysis provided valuable insight.

There is, however, one caveat and that is termed saliency. It might be the case that simple individual audits had a very large and very unusual problem in the recent past. This unusual event could bias the estimate because that recent problem is salient in the mind of the estimator.

After test for a recent, salient, event LOE was accepted as the better choice. The conclusion of all involved was that LOE, while imprecise, was a much better reflection of resources consumption than the highly precise “number of” returns driver.

It is better to be roughly right than precisely wrong!

Comments