Few people outside of the federal government know that a manager can be sent to jail for poor budget management! This has significant behavioral impact and enables something I call hierarchical slack.

The Anti-Deficiency Act(31 U.S.C. § 1341), known as the ADA, makes it a crime to overspend an appropriation and the responsible party is subject to fines and/or imprisonment for doing so. The original intent was laudable.

The law prevents an outgoing administration to make financial commitments that spend resources of the incoming administration. However, it also has unintended consequences.

Behavioral Implications in Budget Execution

To my knowledge no one has ever gone to jail for an ADA violation. Yet, its impact on federal accounting and management is profound. Management information systems and management practice closely track expenditures and obligations against appropriated and authorized levels. Relatively little effort is spent reviewing how the funds are spent.

The emphasis is on spending all budget without overspending and the resulting definition of good financial management is spending 99.9% of the budget. In fact, organizations work hard, and sometimes frantically, on spending in the last weeks and days of a fiscal year to expend or obligate all current year funds right up the limit.

Why? Well, we want to avoid an ADA violation next year too!

Behavior Implications in Budget Formulation

There are also great incentives to build future budgets that are very conservative. That is to say easily achievable. Managers subject to severe personal penalties are unlikely to set targets that stretch organizational performance. That would be an unnecessary personal risk.

Note that easily achievable plans are not generally considered good in the private sector. Companies often use their budgets and plans to put pressure on the manager and organization to perform. Not that failure is the goal, but plans that are never missed seldom result in the best possible performance and are not good either.

So it is easily understandable that managers formulating budget seek to add conservative judgement and over estimates in their plans. This is what I call “slack.” It might not be too bad enough if a major department of the federal government built a 10% slack into its budget to cover unforeseen contingencies.

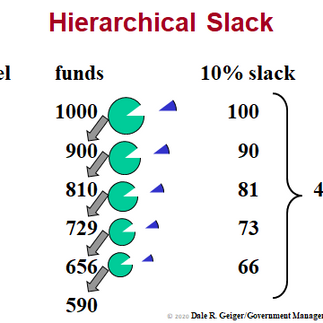

However, every level in the chain of command in the hierarchy may feel the same pressure to avoid exceeding the budget. If every level in an organization chart with five levels plans a 10% slack the impact is remarkable.

The illustration shows the 1st level taking 100 slack out of their 1000 budget. Level 2 then has a budget of 900 and taking 10% slack means 90 of conservatively planned resources Level 3 then gets a budget of 810 and takes 81 and so forth.

As the illustration shows, five levels taking 10% slack at each level means that the department has a total of 410 in slack. If so, only 590 of the original 1000 may be realistically planned!

Perhaps it should not be surprising that no one has gone to jail in the history of the Anti-Deficiency Act. It should also not be surprising that there are many opportunities for performance improvement and increased cost effectiveness.

Comments